Like most investors, you have probably learned the most important thing you need to know about a stock is its price-to-earnings (P/E) ratio.

Well… get ready for a big surprise, particularly for the most successful stocks of the last 100+ years.

For ages, analysts have used P/E ratios as their basic measurement tool in deciding whether a stock is undervalued (low P/E) and should be bought or is overvalued (high P/E) and should be sold.

William O’Neil’s (Investors.com, CAN SLIM) ongoing analysis of the most successful stocks from 1880 to the present reveals that, contrary to most investors’ beliefs, P/E ratios were not a relevant factor in price movement and have very little to do with whether a stock should be bought or sold. O’Neil suggests that a high P/E ratio is an outcome of strong earnings growth, which in turn attracts large institutional buyers leading to significant price performance. Hence, primary consideration should be given whether the rate of change in earnings is substantially increasing or decreasing.

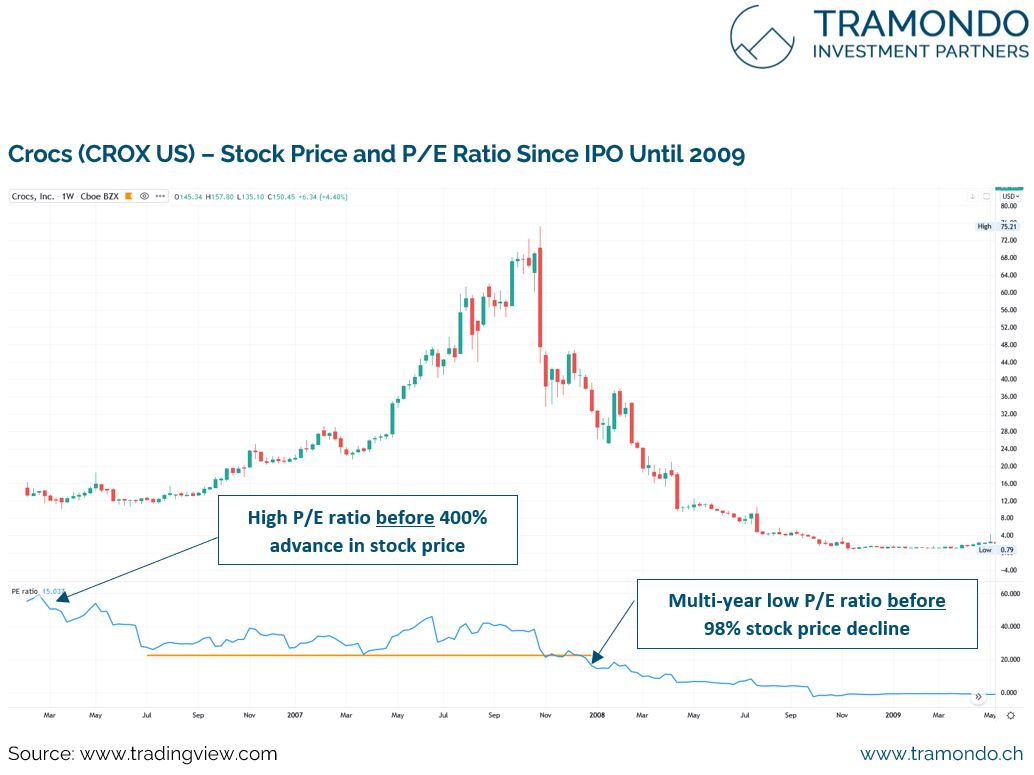

The best performing stocks of the 1990s had P/E ratios of 31 before their large price moves. These ratios further increased to the 70s range during their subsequent stock price rise. For instance, Google’s P/E ratio (Chart 1) was already in the 150s when its stock price moved up from $50 a share in 2004 to $370 in 2008. Crocs’ P/E ratio (Chart 2) was above 60 before a 400% stock advance and at multi-year lows before a 98% decline in stock price.

Therefore, investors with a bias against what they consider to be high P/E ratios will miss out on some of the greatest opportunities of this or any other time. Moreover, the wide P/E ranges were rather found to occur because of roaring bull markets and severe bear markets. Pure reliance on P/E ratios thus often ignores more basic trends such as cycles, general market conditions, events, other asset classes, psychology and sentiment.

At Tramondo, we never buy a stock just because the P/E ratio makes it look like a bargain. There are usually good reasons why the P/E ratio is low – even if you compare it within a sector and among peers. Often, earnings are showing a material deceleration which justify a lower valuation. We believe that the market does not really work in such a scientific way. Just because some set formula might indicate that a stock should be purchased does not necessarily mean the supply and demand which follow will reflect the anticipated value. Opportunity costs are not to be neglected as highlighted by Gerald M. Loeb (The Battle for Investment Survival, 1935) as this thinking can cost an investor serious profits, in particular during bull markets.

Indeed, high-P/E stocks will be more volatile, particularly in the high-tech area and they can temporarily get ahead of itself (Stock Price Maturation Cycle), but the same can be said for lower-P/E stocks. We can relate with the adage “valuation (in form of P/Es or other metrics) matters but only afterwards”.

In summary, earnings and sales growth are simply the key fundamental factors which have contributed the most to total shareholder gains over time (Chart 3).