10 July 2019

Highlights of the current issue

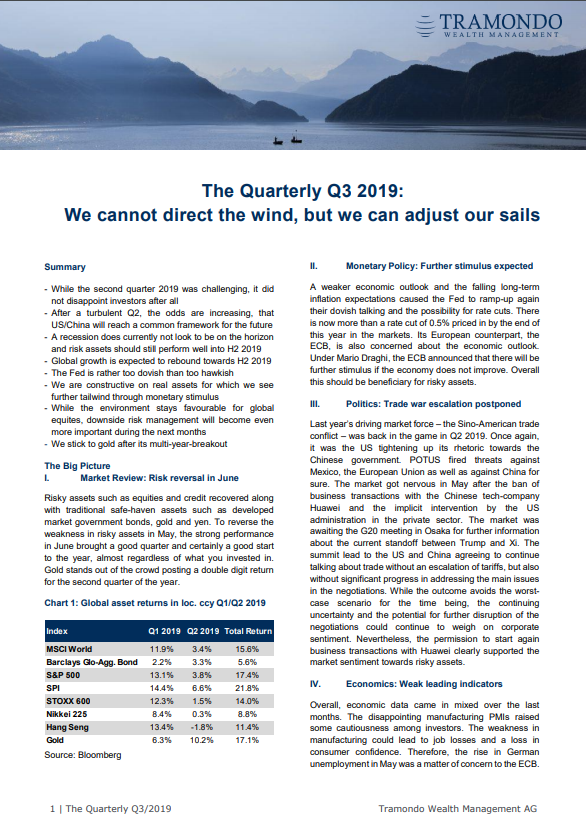

- While the second quarter 2019 was challenging, it did not disappoint investors after all

- After a turbulent Q2, the odds are increasing, that US/China will reach a common framework for the future

- A recession does currently not look to be on the horizon and risk assets should still perform well into H2 2019

- Global growth is expected to rebound towards H2 2019

- The Fed is rather too dovish than too hawkish

- We are constructive on real assets for which we see further tailwind through monetary stimulus

- While the environment stays favourable for global equites, downside risk management will become even more important during the next months

- We stick to gold after its multi-year-breakout